The evolution of the photovoltaic market was distorted by its own bubble that led to huge investments, and that after it burst (2008-2012) needed restructuring.

However, since 2013, the solar market has been experiencing very rapid and uninterrupted growth, resulting from an extraordinary reduction in photovoltaic energy costs, from ~2€/Wp in 2011 to ~0.25€/Wp by the end of 2018. This reduction of such an order of magnitude in the last 8 years made photovoltaic generation even cheaper than nuclear generation or that derived from fossil fuels.

In February 2018, ACWA Power won a 300 MW tender in Saudi Arabia at a record price of 2.34 US cents/kWh. Even more impressive is that in that tender, 7 of the technical bids were less than 2.9 US cents/kWh. In other words, the new tariff range of 2 US cents was established as the standard price under ideal conditions, in locations with high irradiation and a stable political framework.

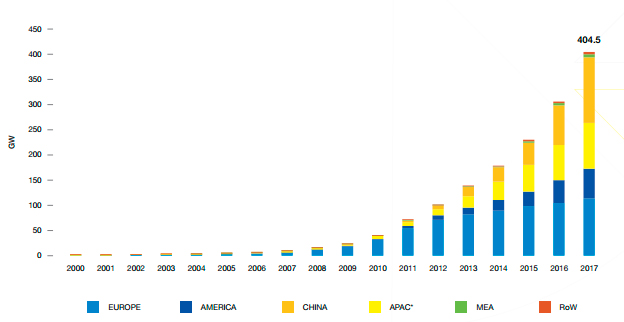

Market projections for the photovoltaic sector are for sustained long-term growth, although growth is expected to moderate mainly due to China’s reduced capacity. As can be seen in Illustration 19, each year around 120 new GW of photovoltaic power are installed worldwide, almost 50% of which is installed in Asia.

According to SPE, under optimal conditions, the accumulated photovoltaic generation capacity worldwide could reach 1,270 GW by the end of 2022, but they consider it more likely to remain at around 1,026 GW. Even so, that would mean that solar energy would reach the cumulative power level of terawatts (TW) by 2022.

The outlook for the world’s largest photovoltaic markets will generally be very positive for the coming years. Most of the top 20 markets will see double-digit annual growth rates until 2022 and at least two countries will grow even more than 100%, Egypt and Saudi Arabia.

Good forecasts for the photovoltaic sector allow us to estimate investment needs in production equipment, which will eventually lead to sales of lines around the world. Also, the spectacular increase expected in the middle-east and Latin America may also be seen.

KONIKER, thanks to its close collaboration with Mondragon Assembly, has extensive experience in the development of innovative production processes, as well as in their design and simulation, which allows it to respond to the evolution of photovoltaic module cells and architectures.

Koniker’s research areas are focused on the entire production chain of the photovoltaic module, from product technologies to manufacturing technology:

- Development of new Tabber Stringer machine architectures. New methods of interconnection are being investigated, such as conductive adhesives (ECA) or Back Contack technologies.

- New module technologies: Modules for extreme conditions such as in the desert, glass-glass modules, bi-facial modules, shingling modules, etc.

- Research into new lamination methods.

- Profiling for the manufacture of supports and structures.

- Inspection of modules: Use of artificial intelligence (Machine and Deep Learning) for quality control by electro-luminescence

- Use of Industry 4.0 technologies for process controls and efficiency management of the production line.